Two Harbors Investment Corp. (TWO) is the highest-yielding stock in the more aggressive ?pushing-the-envelope? version of the StockScreen123 Prudent Yield Hog model I wrote about on March 3.

Brace yourself. With a 14.2% yield in this day and age, you have to expect something way out of the ordinary. I?ll tell you up front, not every prudent-yield-hog situation is going to look like this one, but I figure you?d like to get the lowdown on a 14.2% yield sooner rather than later. So here goes:

This is a new firm, launched in 2009. It invests in mortgage-related securities, and management plans to make sure its investments and dividend policy conform to REIT requirements.

- Mortgage-related securities constitute the highest-risk REIT sub-segment, the one at the epicenter of the global financial crisis. So this line of business is about as comforting as driving a gasoline tank truck through a forest fire and should, in and of itself, push the yield up toward the top of any yield-hog universe. But in this case, there?s more . . .

- The firm is very new, having only a one-year track record as a publicly-traded entity.

- The firm came public via the reverse takeover method that has become so famous, or infamous if you prefer, as a result of many Chinese businesses that chose this way to get access to the U.S. equity market. (Speaking for myself, I?m not down on the process, but many others are and given the dynamics of supply and demand, the trading choices of the majority are going to make themselves felt in stock price levels, and in cases like this, yield.)

That was quick. We see can easily see what the risks are, why Mr. Market is giving about ten percentage points worth of yield above and beyond what we generally see today among REITs, and even a few points above what we typically see for higher-risk mortgage REITs.

Actually, did you notice above, how many extra words I used to refer to this entity as a REIT? There was a reason for that. Legalistically, this is, in fact, a REIT. But for all practical purposes, you can think of it as a hedge fund that emphasizes relative value in the distressed mortgage-securities sector.

I don?t use the phrase ?hedge fund? lightly. The key executives, here, including the two co-Chief Investment Officers, come from a hedge fund firm known as Pine River, which had more than $3.4 billion under management as of late 2010, and a specialty in mortgage securities. The Two Harbors loan portfolio is managed by a Pine Rivers subsidiary set up for that purpose. So a stake in this REIT can be seen as the functional equivalent of an investment in a hedge fund (without the hedge-fund fee structure).

The investment personnel here are Wall Street veterans who have been investors and traders in fixed income in general and mortgage-backed securities in particular. It?s easy for armchair gurus to preach against a bunch of guys who seem to have had their hands on or near the controls as the market careened downward. But if we?re going to pursue yield, we?ll need to check our judgmental tendencies at the door. The hard-boiled view, the one we?ll need to adopt, recognizes that booms and busts happen all the time in all kinds of markets and that when busts occur, it can be a heck of a lot more profitable to grab opportunities rather than to point fingers.

In pursuing opportunities, TWO takes a holistic view of the mortgage-backed market. It goes wherever is believes the values are, whether in agency securities or non-agency, fixed rate or adjustable, derivatives, etc. It uses a disciplined asset-selection approach in an effort to balance interest-rate risk, credit risk, and prepayment tendencies.

Data released by TWO in the 2010 fourth quarter shows the following:

- The Leverage ratio (defined by TWO as borrowings to fund purchases of residential mortgage-backed securities divided by equity) was 3.3 as of 9/30/10, versus a peer average of 5.6 (TWO?s leverage dropped to 2.5 by December 31st)

- �For every 1,000 basis point change in interest rates, TWO estimates its 9/30/10 equity value would rise or fall by 4.5%, (2.1% by December 31st) versus a 13.9% peer average, thus indicating considerably lower interest-rate exposure

- At 9/30/10, TWO estimates the prepayment rate of the mortgages upon which its portfolio is based at 9.7% (8.0% by December 31st), versus a peer average of 21.9%

The yield on TWO?s actual portfolio was 5.8% in the fourth quarter of 2010 (3.8% from agency securities and 11.4% from non-agency securities). Obviously, that?s not going to all be passed on to REIT shareholders penny for penny; there are REIT expenses. But it should give you some idea more or less of what TWO?s yield could look like if not for the risk-premium that pushes its stock down.

In its first year of operation, TWO has shown itself to let the dividend reflect available funds: the payouts for 2010 were $0.36 for the first quarter, $0.33 for the second, $0.39 for the third, and $0.40 for the fourth. If we assume the $0.40 quarterly payout persists in 2011, this would suggest a yield of 14.2% on the stock.

That?s not a crazy assumption. Remember, the yield on TWO?s actual portfolio is 5.8%, a number that is not outrageously eye-catching. As noted, the huge yield on TWO stock comes mainly from the fact that investors haven?t, to date, been willing to pay up for the dividend stream, even relative to what we see with depressed prices for other mortgage REITs.

I just want to make one more observation about the impact of the short history on the rank used in the Prudent Yield Hog model. It has a growth component. Some factors are distorted upward by super-high growth rates as revenues etc. go from near-zero to a normal level. More items are distorted lower as the short history causes TWO?s rank to be punished by NA (Not Available) scores for other growth factors. Note, though, that, if I were to completely eliminate the growth part of the model, TWO would still rank in the mid-80s, way above the 40 threshold needed to pass muster.

This is something of an idiosyncratic investment idea, but shareholders are well compensated in the form of a very high yield (a yield high enough to accommodate some payments below $0.40 in the year ahead) for taking an edgy position that?s one of 15 in a model that gets refreshed every three months.

APPENDIX

The Prudent Yield Hog model, created on StockScreen123 and introduced in a 3/1/11 Seeking Alpha article, is based on the notion that income-seekers can achieve satisfactory returns by reaching for the highest possible yields if they work with a list that has been pre-qualified to eliminate companies that bear the greatest risk of dividend cut or elimination.

It uses a screen that contains the following rules:

- Basic Universe Definitions

o Eliminate OTC stocks, stocks trading below $5, stocks with market capitalization below $250 million, ADRs and companies classified as Miscellaneous Financial Services (most of which are closed-end mutual funds)

o Daily volume over the past 60 days must have averaged at least 50,000 shares

- Yield must be equal to or greater than 2/3 of the rate on the 10-year Treasury

- Yield may not exceed 5 times the rate on the 10-year Treasury

- For this pushing-the-envelope version of the model, the stock must rate 40 or better on a scale of zero to 100 under a ranking system designed to evaluate high-yielding income stocks; under the default version, it would have to rate at least 60

Here?s a summary of the ranking system referred to in the last screening rule:

- Growth Profile (one third of the score)

o Dividend growth (60% of sub-category)

o EPS growth (30%)

o Sales growth (10%)

- Dividend Security (one third of the score)

o Trailing 12 month dividend payout ratio (lower is better) sorted relative to industry peers

- Investor Sentiment (one third of the score)

o Price signals (30% of sub-category)

o Technical Signals (30%)

o Investor Comfort (40%)

For further details, click here.

From the list of passing companies (i.e., those that have been successfully pre-qualified), select the 15 highest-yielding stocks.

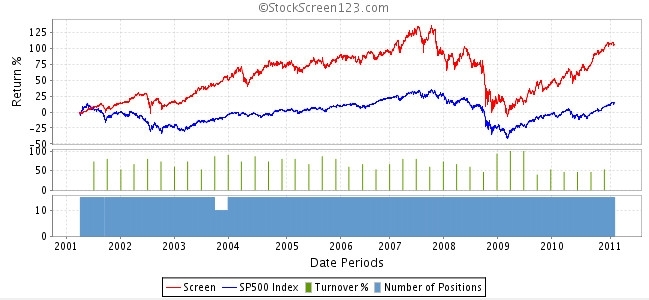

Figure A-1 (click to enlarge) shows backtested price performance of the strategy from 3/31/01 ? 2/28/11 assuming the model is re-run and the list refreshed every three months.

Figure A-1

That?s price performance only. The model faltered during the financial crisis of 2008, as did most other strategies. But the overall start-to-finish capital gain was 106.7%; or 7.6% annualized, which would be added to the yield, which was often in the neighborhood of 9%.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in TWO over the next 72 hours.

Powered By iWebRSS.com